Picture this: You’ve poured your soul into a business idea—a sleek e-commerce site for artisanal coffee gear, or a mobile app solving urban parking woes. Prototypes gleam, customers buzz on social media, but your bank account echoes empty. Banks demand two years of revenue statements you don’t have. Sound familiar? You’re not alone. For entrepreneurs with under 24 months of revenue history, traditional loans feel like a mirage.

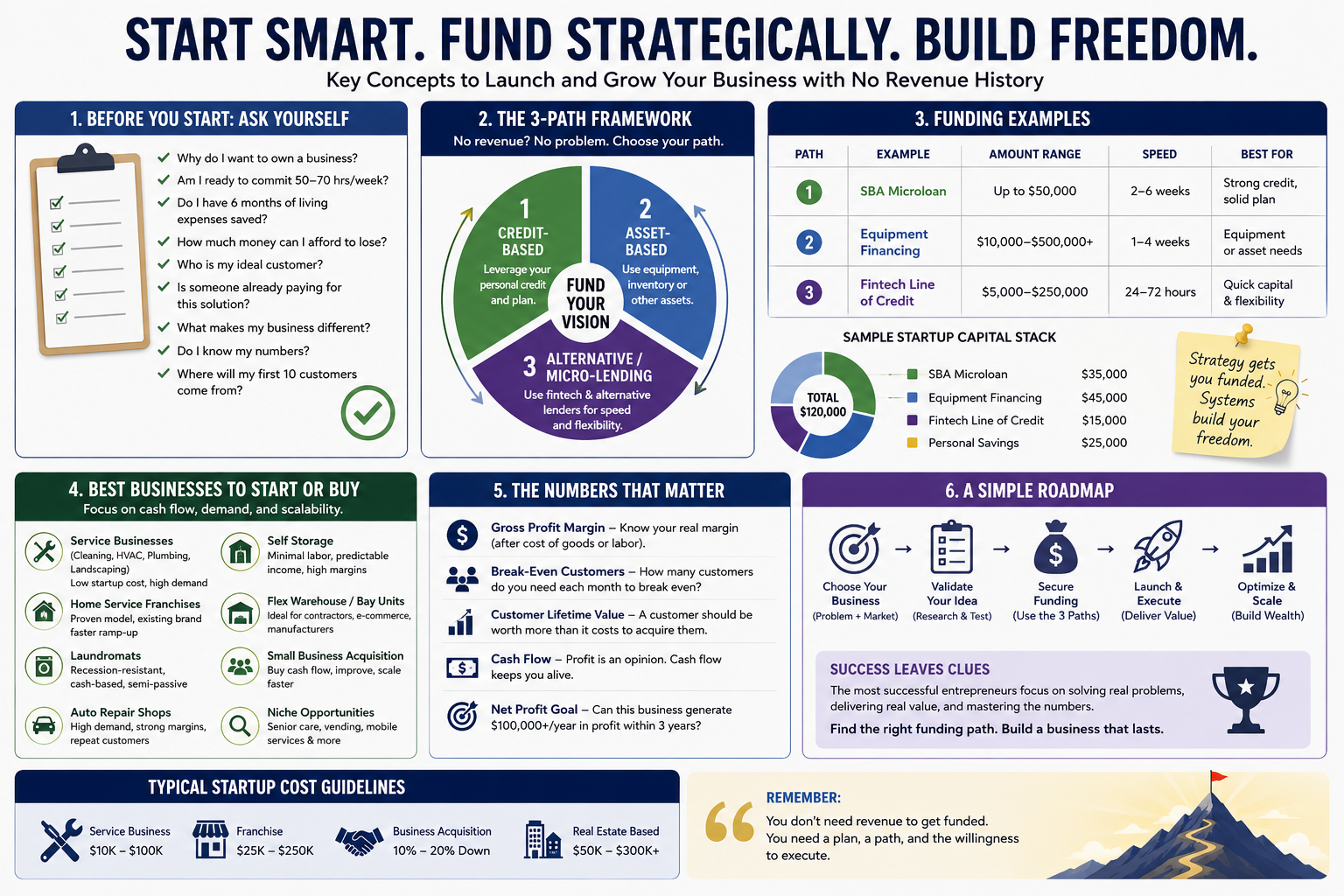

But here’s the truth—no hype, just systems that work. Funding for new businesses exists beyond revenue-proof walls. Enter the 3-Path Framework for startup business loans no revenue needed. This isn’t a scattershot hunt for miracles. It’s a structured map: Path 1 (Credit-Based), Path 2 (Asset-Based), and Path 3 (Alternative/Micro-Lending). Each path offers business financing for startups with clear entry points. Find the right funding path, and watch doors swing open.

Path 1: Credit-Based Funding – Leverage Your Personal Foundation

When revenue is zero or sparse, lenders pivot to you—the founder. Credit-based startup business loans hinge on your personal credit score (ideally 680+), often with a personal guarantee. This path shines for solopreneurs or micro-teams with solid personal finances but unproven business traction.

The star here? SBA microloans. Backed by the Small Business Administration, these deliver up to $50,000 through nonprofit intermediaries. No revenue minimum—just a viable plan and your credit as collateral.

Practical Steps to Secure Credit-Based Loans

- Check and Boost Your Score: Pull free reports from AnnualCreditReport.com. Dispute errors. Pay down debts to hit 700+.

- Build a Lean Business Plan: Outline market need, revenue model, and milestones in 10-15 pages. Tools like LivePlan streamline this.

- Target SBA Microloan Providers: Use the SBA’s lender match tool. Local CDFIs (Community Development Financial Institutions) often approve faster for underserved founders.

- Prepare Guarantee Docs: Expect UCC filings or liens on personal assets. Shop rates—expect 8-13% APR.

- Apply in Waves: Submit to 3-5 lenders simultaneously. Track with a simple spreadsheet.

One founder swapped rejection letters for a $25,000 SBA microloan by emphasizing personal FICO strength. Systems like this turn personal grit into business fuel.

Path 2: Asset-Based Lending – Collateral Speaks Louder Than Revenue

Got equipment needs? Inventory to stock? Asset-based funding for new businesses ignores revenue history entirely. Lenders advance against the assets themselves—think machinery, vehicles, or goods. It’s perfect for product-heavy startups like manufacturers or retailers bootstrapping scale.

Rates hover 10-20%, but terms stretch 2-5 years. No personal guarantee required if assets suffice. This path funds business financing for startups poised for quick asset deployment.

Practical Steps for Asset-Based Funding

- Inventory Your Assets: Appraise equipment via Kelley Blue Book or professional valuators. Aim for 1.5x loan-to-value ratio.

- Select Lenders: Equipment financiers like Balboa Capital or Crest Capital specialize in no-revenue deals.

- Gather Proof: Invoices, photos, serial numbers. For inventory, provide vendor quotes.

- Negotiate Terms: Seek floating rates tied to assets. Avoid balloon payments.

- Monitor Usage: Use funds strictly for listed assets to maintain compliance.

Assets don’t lie about cash flow potential—they prove it. Find the right funding path here, and revenue follows naturally.

Path 3: Alternative Lending and Fintech – Speed Meets Flexibility

For lightning-fast capital, dive into alternative lending and fintech loans. Platforms like Kabbage (now Amex), Fundbox, or Bluevine assess bank connections, cash flow projections, and even social proof over revenue history. Amounts from $5,000-$250,000 fund marketing blitzes or hires.

Micro-lending arms, including Kiva’s 0% interest peer model, cater to diverse founders. Approval in 24-72 hours—no branches, all digital.

Practical Steps to Tap Alternative Sources

- Link Accounts: Connect business bank (even if new) and Plaid-enabled apps.

- Show Traction: Upload website analytics, pre-orders, or customer emails.

- Compare Platforms: Use NerdWallet or LendStreet for side-by-side APRs (15-50%).

- Start Small: Secure $10K line first to build repayment history.

- Automate Repayments: Daily/weekly draws prevent defaults.

No hype, just systems that work. Fintechs have greenlit thousands of startups, turning beta tests into breakouts.

Choosing Your Path: The Systems Audit

Not every path fits every venture. Audit yours: Strong credit? Path 1. Assets ready? Path 2. Need speed? Path 3. Often, blend them—SBA for core, fintech for growth. Track metrics: approval odds, costs, timelines. Consult free SBA counselors via SCORE.org.

This 3-Path Framework demystifies funding for new businesses. No revenue? No problem. Systems outperform hope every time.

Launch Without Limits

Your startup’s ignition switch isn’t revenue—it’s strategy. Armed with this framework, sidestep gatekeepers. Find the right funding path, ignite your vision, and build the empire. The universe rewards the prepared. What’s your first step?

Hypothetical Story: How Sarah Used the 3-Path Framework to Launch a Business

Meet Sarah.

Sarah is a 42-year-old project manager earning $75,000 per year. She has a 720 credit score, $25,000 in savings, and dreams of leaving corporate America.

She wants to start a business that generates cash flow quickly rather than spending years developing an app.

After researching hundreds of startups, she discovers a simple truth:

The easiest businesses to fund are businesses with assets, recurring revenue, or proven demand.

Step 1: Evaluate Funding Options

Sarah has:

- Credit Score: 720

- Savings: $25,000

- No business revenue

- No investors

She decides to pursue all three funding paths simultaneously.

Path 1: SBA Microloan

She creates a simple business plan and applies through a local SBA microloan provider.

Result:

- Approved for $35,000

- 9% interest

- 6-year term

Path 2: Asset-Based Financing

She wants equipment for the business.

The equipment vendor offers:

- $50,000 equipment financing

- 10% down payment

Result:

- Sarah puts down $5,000

- Finances $45,000

Path 3: Fintech Working Capital

She opens a business checking account and builds a website.

After showing pre-orders and contracts, she qualifies for:

- $15,000 business line of credit

Total Capital Raised

| Source | Amount |

|---|---|

| SBA Microloan | $35,000 |

| Equipment Financing | $45,000 |

| Fintech Line | $15,000 |

| Personal Savings | $25,000 |

| Total Available Capital | $120,000 |

Sarah now has access to $120,000 despite having zero business revenue.

What Business Should She Start?

Many new entrepreneurs make a costly mistake.

They ask:

“What business am I passionate about?”

Instead, ask:

“What business can generate cash flow fastest?”

Best Business Types for New Entrepreneurs

Option 1: Service Businesses (Lowest Risk)

Examples:

- HVAC

- Plumbing

- Roofing

- Landscaping

- Cleaning

- Mobile Auto Repair

Startup Cost

$20,000–$100,000

Why Lenders Like Them

- Immediate revenue

- Low inventory

- High demand

- Easier to scale

Example

Sarah buys a small cleaning company generating:

- Revenue: $15,000/month

- Profit: $4,000/month

Purchase Price:

- $60,000

Using her funding, she buys the company and begins generating cash flow on Day 1.

Option 2: Home Service Franchise

Examples:

- Junk Removal

- Painting

- Pressure Washing

- Senior Care

Startup Cost

$75,000-$250,000

Benefits

- Proven system

- Existing brand

- Easier financing

Option 3: Laundromat

One of the most lender-friendly businesses.

Startup Cost

$100,000-$500,000

Why

- Mostly cash flow

- Recession resistant

- Semi-passive

Example:

Sarah purchases a laundromat generating:

- Revenue: $18,000/month

- Expenses: $8,000/month

- Cash Flow: $10,000/month

Option 4: Self Storage

Startup Cost

$250,000-$2,000,000+

Why

- Minimal labor

- Predictable income

- High margins

Many investors use SBA loans and private money together.

Option 5: Small Auto Repair Shop

This is one of the most overlooked opportunities.

Example

Purchase Price:

$350,000

Down Payment:

10%

Loan:

$315,000

Annual Cash Flow:

$100,000+

The owner can often replace their job income within the first year.

Option 6: Flex Warehouse Units

This is becoming one of the hottest commercial real estate niches.

Examples:

- Contractors

- Electricians

- Landscapers

- Online sellers

- Small manufacturers

A 2,000-square-foot bay renting for $2,500/month can generate substantial recurring income once occupied.

How Much Money Do You Really Need?

Many people think they need:

- $250,000

- $500,000

- $1,000,000

Often they don’t.

Service Business Startup

Recommended Cash:

- $10,000-$25,000

Existing Business Acquisition

Recommended Cash:

- 10%-20% down payment

Small Franchise

Recommended Cash:

- $25,000-$75,000

Commercial Real Estate

Recommended Cash:

- $50,000-$300,000+

Sarah’s Outcome

Instead of building a speculative app, Sarah purchases a small cleaning company.

Year 1

- Revenue: $180,000

- Profit: $50,000

Year 2

- Revenue: $320,000

- Profit: $110,000

Year 3

- Revenue: $500,000

- Profit: $180,000

She leaves her corporate job and begins buying additional service businesses.

The Real Lesson

The fastest path to wealth is often buying an existing cash-flowing business rather than starting from scratch.

For entrepreneurs with little or no business revenue history, the most financeable opportunities are usually:

- Service businesses

- Existing small businesses

- Laundromats

- Auto repair shops

- Self-storage facilities

- Flex warehouse developments

- Home-service franchises

The goal isn’t simply getting a loan. The goal is using that loan to acquire or build an asset that starts producing cash flow immediately. That’s how entrepreneurs move from chasing funding to building wealth.

Absolutely. One of the biggest reasons businesses fail is not lack of funding—it’s that the owner never asked the hard questions before they started.

I call this the “Business Readiness Checklist.”

If someone answers “No” to more than 5 of these questions, they probably need more planning before investing money.

Part 1: Personal Readiness

Why do I want to own a business?

- More income?

- More freedom?

- Build wealth?

- Leave a legacy?

- Escape a job?

If the answer is simply “I hate my boss,” that’s usually not enough.

Am I willing to work 50-70 hours per week for the first 1-3 years?

Most startups demand significant time before they provide freedom.

Can my family support this decision?

- Spouse support?

- Time commitment?

- Financial stress?

Many businesses fail because of family conflict, not business problems.

How much money can I afford to lose?

Never invest money you can’t afford to lose.

Do I have six months of personal living expenses saved?

If not, every slow month becomes a crisis.

Part 2: Market Validation

What problem am I solving?

Customers buy solutions, not products.

Who is my ideal customer?

Be specific:

- Homeowners?

- Real estate investors?

- Restaurants?

- Contractors?

Is somebody already paying for this solution?

If nobody is paying for a similar solution today, that’s a warning sign.

How large is the market?

Can you realistically find 100 customers?

1,000 customers?

10,000 customers?

What makes my business different?

Better service?

Lower cost?

Faster delivery?

Convenience?

Specialized expertise?

Part 3: Financial Reality

How much money do I actually need?

Break down:

- Equipment

- Inventory

- Rent

- Payroll

- Marketing

- Insurance

- Working capital

How long before I become profitable?

Most new owners underestimate this by 50%.

How many customers do I need each month to break even?

Example:

Monthly expenses = $8,000

Average profit per customer = $400

Break-even = 20 customers

Do I know my gross profit margin?

Many people know sales.

Few know margins.

Margins determine survival.

Where will my first 10 customers come from?

This question alone eliminates many bad business ideas.

Part 4: Operational Readiness

Can I explain my business in 30 seconds?

If not, customers probably won’t understand it either.

What skills do I already have?

Sales?

Management?

Construction?

Marketing?

Accounting?

What skills am I missing?

Every successful owner knows their weaknesses.

Can the business operate without me?

If not, you’ve bought yourself a job.

Do I have a written process for delivering my product or service?

Systems create scalability.

Part 5: Funding Readiness

What is my personal credit score?

Most startup funding starts here.

How much cash can I contribute?

Lenders want to see owner investment.

What collateral do I have?

- Home equity

- Equipment

- Vehicles

- Investment accounts

Which funding path fits me?

Path 1: Credit-Based

- 680+ credit score

- Little collateral

- Small startup

Path 2: Asset-Based

- Equipment

- Inventory

- Real estate

Path 3: Alternative Funding

- Need speed

- Growing quickly

- Short-term capital needs

Part 6: Business Acquisition Questions

Before buying an existing business, ask:

Why is the owner selling?

Retirement?

Burnout?

Financial trouble?

Can I verify the financials?

Review:

- Tax returns

- Bank statements

- Profit & Loss statements

What would happen if the owner left tomorrow?

Will customers stay?

Will employees stay?

Is revenue recurring?

Recurring revenue is far more valuable than one-time sales.

Can I improve the business quickly?

Look for opportunities such as:

- Better marketing

- Better pricing

- Better customer service

- Better technology

The Most Important Question

Before starting any business, ask:

“Can this business realistically produce $100,000 per year in profit within 3 years?”

If the answer is no, or you don’t know, keep researching.

The most successful entrepreneurs don’t start with a product. They start with a market need, a clear profit model, and a plan to reach customers.

For many first-time entrepreneurs, buying a small cash-flowing business (service company, laundromat, auto repair shop, storage facility, etc.) is often less risky than launching a brand-new startup because customers and revenue already exist.