Imagine this: You’ve got a solid business plan, recurring customers lining up, and a clear path to scale. But when you walk into your bank for that SBA 7(a) loan everyone’s talking about, you’re met with a wall of paperwork, three-month waits, and a rejection letter citing “insufficient collateral.”

In the realm of small business funding, various avenues exist to secure the necessary capital.

Understanding the small business funding options available today is crucial for growth.

This guide to small business funding showcases various choices for entrepreneurs.

Let’s explore the landscape of small business funding in detail.

We’ll assess the small business funding pathways available today.

Familiarizing yourself with small business funding options is key to making informed choices.

Discover the landscape of small business funding that fits your needs.

The funding landscape has shifted dramatically. Bank loans are no longer the default—or even the best option. Heading into 2026, new players, innovative models, and untapped opportunities are reshaping how small businesses fuel growth.

Current trends in small business funding reveal significant shifts in the market.

Understanding the challenges of small business funding is essential to success.

Many entrepreneurs face hurdles in small business funding due to outdated methods.

A deeper understanding of small business funding can lead to better decisions.

Industry insights on small business funding highlight important trends.

Keeping informed about small business funding options can enhance your strategy.

Most owners still default to what their banker pitches. But that’s a mistake. This small business funding roadmap for 2026 reveals eight practical pathways beyond traditional loans—each with real-world fit, terms, and pitfalls to avoid.

Consider how different small business funding methods align with your goals.

Each small business funding option has unique features that can suit your needs.

A Quick Overview: Your 2026 Funding Roadmap

Explore various routes of small business funding to tailor to your strategy.

Each of these small business funding options has its specific advantages.

Choosing the right small business funding is vital for growth.

Many entrepreneurs find success through diverse small business funding strategies.

We’ll break it down step by step: why banks are fading, the eight core alternatives with pros and cons, a simple decision framework, deadly mistakes to dodge, and trends to watch.

Integrating small business funding options can lead to a comprehensive strategy.

By the end, you’ll know exactly which path fits your business—whether you’re a SaaS founder needing quick cash flow or a service pro with zero assets to pledge.

Let’s dive in. No fluff, just actionable intel for founders like you.

Expanding your knowledge of small business funding helps navigate the landscape.

Make informed decisions when pursuing small business funding to ensure success.

Effective strategies for small business funding can drive growth and sustainability.

Understanding your options in small business funding is critical for entrepreneurs.

Choosing between small business funding routes can maximize your potential.

Business owners need to understand small business funding to scale effectively.

Why Traditional Bank Loans Are Losing Their Grip

Exploring small business funding avenues enhances your financial strategy.

Make the most of available small business funding to achieve your goals.

Deciding on the right small business funding strategy can lead to growth.

Smart entrepreneurs leverage small business funding to enhance their operations.

Big banks approve fewer than 25% of small business loan applications. That’s not a rumor—it’s the reality from recent Federal Reserve data.

Implementing small business funding effectively can yield significant results.

Keep small business funding in mind as you grow your enterprise.

Underwriting drags on for 60-90 days. Your competitor launches a product while you’re still faxing tax returns.

Evaluate how various small business funding options can benefit your business.

Consider the advantages of diverse small business funding approaches.

Review different small business funding avenues to identify what suits you best.

Collateral demands kill deals for service businesses, digital agencies, or e-com stores with inventory but no real estate. Banks want hard assets; most small ops don’t have them.

Meanwhile, the alternative business funding market explodes past $300 billion in 2026 projections. Fintechs, revenue sharers, and niche lenders move at internet speed.

Banks built the old road. But traffic’s rerouted. Smart founders follow the new map.

The 2026 Funding Roadmap: 8 Pathways Beyond Traditional Loans

Here’s the core of your small business funding roadmap for 2026: eight vetted options. For each, I’ll cover what it is, ideal users, typical terms, and balanced pros/cons.

Pick based on your revenue, speed needs, and assets—not hype.

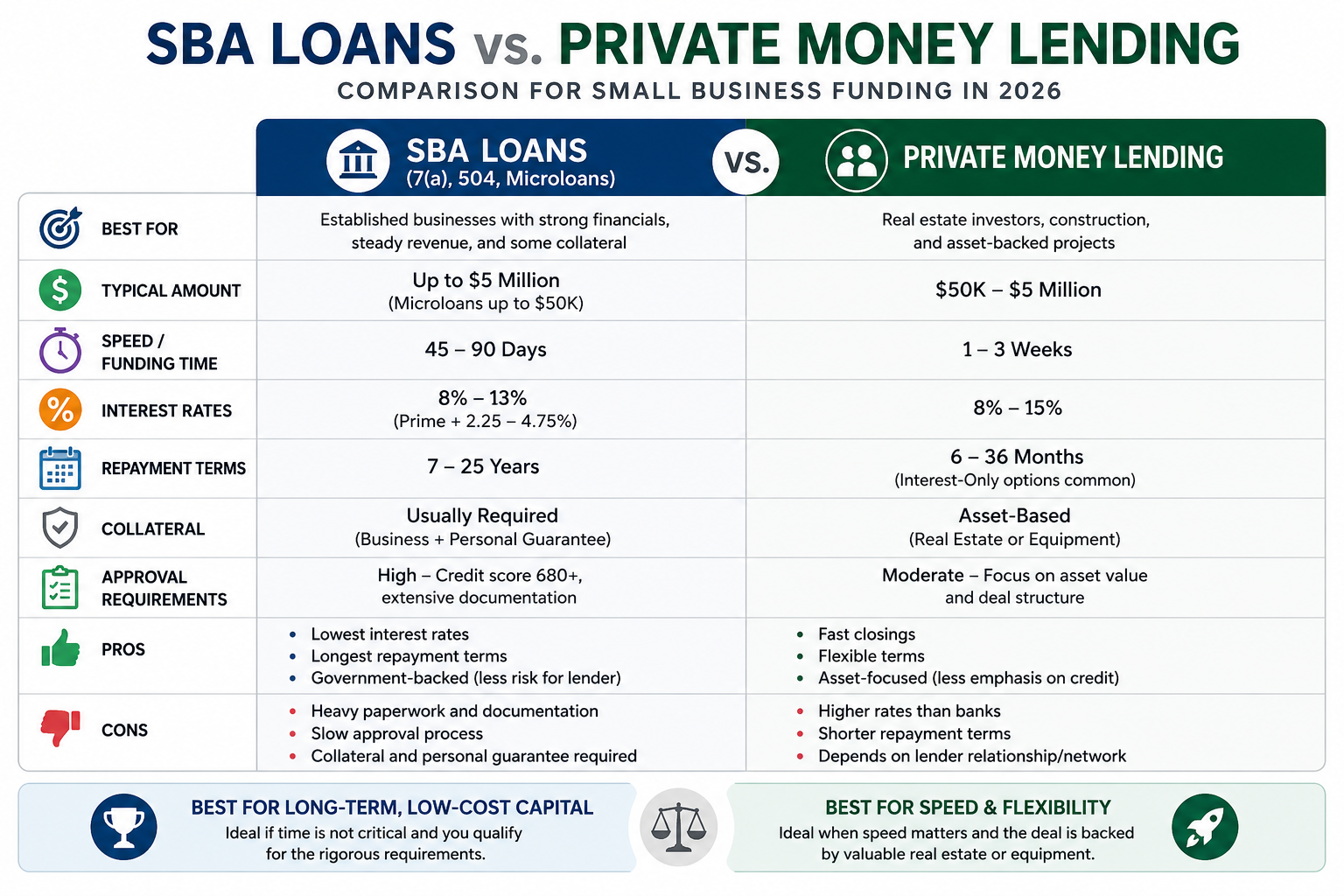

1. SBA Loans (7(a), 504, Microloans)

Government-backed loans through approved lenders. 7(a) for general use up to $5M, 504 for real estate/equipment, microloans under $50K.

Best for established businesses with 2+ years of financials, steady revenue, and some collateral. Not startups.

Terms: 7-25 years, rates 8-13% (prime + 2.25-4.75%). Approval: 45-90 days.

- Pros: Lowest rates, longest terms, partial guarantees reduce lender risk.

- Cons: Intense paperwork, credit score 680+, personal guarantee required. Slow for urgent needs.

Still relevant in 2026 as rates stabilize—but pair with solid bookkeeping via tools like best small business accounting software.

2. Revenue-Based Financing (RBF)

Lenders advance cash repaid as a fixed percentage of monthly revenue. No fixed payments—scales with your sales.

Ideal for e-commerce, SaaS, subscription boxes with $100K+ ARR and predictable MRR. Players: Clearco, Wayflyer, Pipe.

Terms: $10K-$10M advances, 6-18% fee (factor rate 1.06-1.18), repaid over 6-12 months as revenue hits 10-20% slice.

- Pros: No collateral or personal guarantee. Approval in days based on revenue data. Flexible in downturns.

- Cons: Higher effective cost (20-40% APR equiv.). Need bank/API revenue access.

Picture your Shopify store getting $200K for inventory—repaid only when sales flow. Game-changer for growth-stage ops.

3. Online Term Loans & Lines of Credit

Digital lenders offer lump-sum terms or revolving credit. Faster, data-driven approvals.

For working capital gaps, inventory buys. Suits 6+ months in business, $50K+ revenue. OnDeck, Bluevine, Fundbox lead.

Terms: $5K-$500K, 6-24 months, rates 10-60% APR. Lines up to $250K, draw as needed.

- Pros: Funds in 24-72 hours. Minimal docs. Unsecured options exist.

- Cons: High rates for riskier profiles. Daily/weekly debits can strain cash flow.

Check best unsecured business loans for current top picks.

4. Business Credit Cards & 0% APR Stacking

Charge cards or 0% intro cards for short-term funding. Stack multiple for bigger buys.

Underrated for launches, marketing pushes. Needs 700+ personal FICO, established biz.

Terms: Limits $10K-$100K+, 0% APR 12-21 months, then 15-25%. Rewards on spends.

- Pros: Instant access, build credit, rewards. No underwriting hell.

- Cons: Personal liability. High rates post-intro. Discipline required.

Fund a $50K site redesign at 0% over 18 months? Stack two cards, pay from profits. Dive deeper in our best business credit cards guide.

5. Private Money Lending

Asset-based loans from high-net-worth individuals or small funds, not banks. Relationship-driven, flexible.

For real estate flips, construction, equipment-heavy ops with hard assets. Platforms like Medex (medexpmc.com/bc) connect borrowers.

Terms: $50K-$5M, 6-36 months, 8-15% interest. Asset secures; closings in weeks.

- Pros: Speed, negotiable terms, less bureaucracy. Asset focus ignores credit dips.

- Cons: Higher rates than banks. Network-dependent. Foreclosure risk on assets.

One contractor I know closed $300K for a reno in 10 days—bank would’ve taken months.

6. Equipment Financing

Loans or leases where the gear (machinery, vehicles, medical equip) is collateral.

Perfect for manufacturing, trucking, clinics. 90%+ approval if asset qualifies.

Terms: 100% financing, 2-7 years, 6-20% rates. Vendor or specialists like Balboa Capital.

- Pros: High approvals, preserves cash. Tax deductions. Easy upgrades.

- Cons: Limited to equipment. Early payoff penalties sometimes.

Buy that $150K CNC machine today—pay from production gains tomorrow.

7. Crowdfunding & Community Capital

Raise from crowds via equity (Wefunder, StartEngine) or rewards (Kickstarter, Indiegogo).

For consumer products, apps, social missions with audiences. Validate + fund simultaneously.

Terms: $10K-$5M, equity 5-20% or perks. Campaigns 30-60 days; Reg CF up to $5M/year.

- Pros: No repayment. Marketing built-in. Loyal backers become customers.

- Cons: Public failure hurts. Fees 5-12%. Time-intensive campaigns.

8. Grants & Government Programs

Non-repayable cash from feds, states, or corps. SBA grants rare; focus state/minority/women/vet programs.

For R&D, exports, underserved owners. Grants.gov, MBDA hubs.

Terms: $5K-$500K, competitive apps, 3-12 months.

- Pros: Free money. No equity/debt. Prestige boost.

- Cons: Ultra-competitive (<10% win). Strict reporting. Slow.

Free $50K for your green tech startup? Worth the app grind.

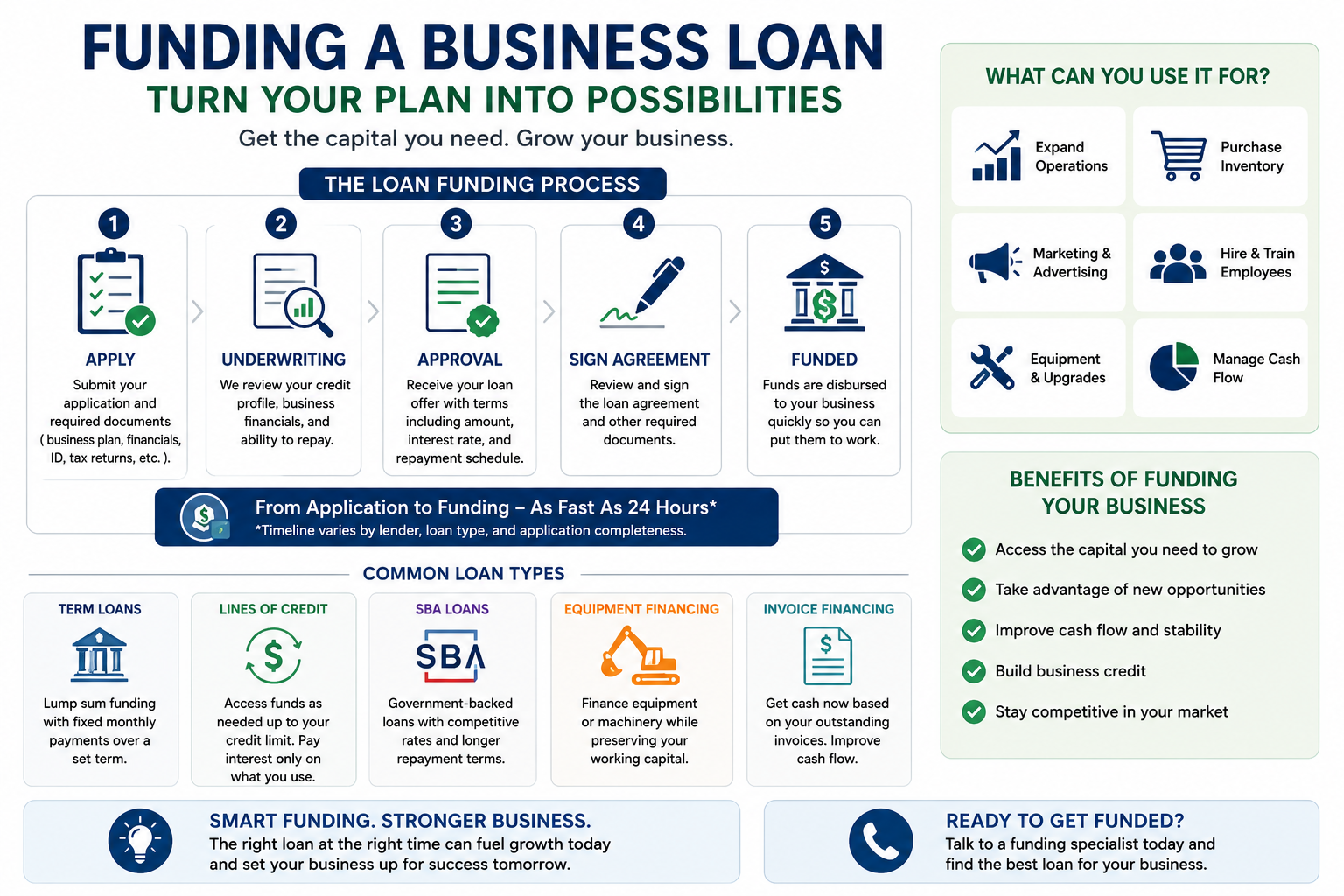

How to Choose the Right Funding Path: The Funding Fit Framework

Overwhelmed by options? Use this four-step framework to nail your small business financing options for 2026.

- Speed check: Need cash this week? RBF or online lenders. Quarter out? SBA or grants.

- Qualification scan: Revenue > $100K? RBF/term loans. Credit 680+? Cards/SBA. Assets? Equipment/private.

- True cost calc: APR matters, but factor speed (time value), covenants, guarantees. $20K RBF at 1.2 factor might beat 12% bank loan delayed 90 days.

- Growth vs survival: Fuel expansion (RBF, equity). Bridge holes? Lines/cards. Never fund losses long-term.

Pro tip: Set up a dedicated business account first. See our picks for best business checking accounts for LLCs.

Run your numbers through it. Clarity emerges fast.

Common Funding Mistakes That Kill Small Businesses

Founders borrow big early, chase shiny objects, and ignore fine print. Here’s how to sidestep the traps.

- Borrowing too much too soon: Scale matches capital. $500K for a $200K/month biz? Cash burn kills.

- Expensive capital for low-ROI: 40% APR debt for a vanity ad campaign? Math doesn’t lie.

- Blind personal guarantees: Your house on the line? Limit exposure.

- No shopping: One lender quote? Leave 20-30% on table.

- APR vs factor confusion: 1.3 factor = ~50% APR. Apples to apples.

Audit your stack quarterly. Founders who do thrive.

2026 Trends to Watch in Business Funding Beyond Bank Loans

Embedded lending hits prime time: QuickBooks, Shopify offer instant loans inside apps.

AI underwriting pulls in alt data—social proof, cash flow patterns—boosting approvals 30%.

Niche platforms rise: Vet-owned funds, green biz lenders, construction specialists.

Banking-as-a-service blurs lines—your neobank becomes your lender.

Stay ahead: Integrate financial tools now for seamless access.

Based on the article you uploaded, here is a clean comparison chart of the 8 funding options discussed.

Small Business Funding Roadmap 2026: Pros & Cons Comparison

| Funding Option | Best For | Typical Amount | Speed | Pros | Cons |

|---|---|---|---|---|---|

| SBA Loans (7a, 504, Microloan) | Established businesses with strong financials | Up to $5M | 45-90 Days | Lowest rates, longest terms, government-backed | Heavy paperwork, collateral requirements, slow approvals |

| Revenue-Based Financing (RBF) | SaaS, E-commerce, Subscription Businesses | $10K-$10M | 2-7 Days | No collateral, payments flex with revenue, quick funding | Higher effective APR, requires consistent revenue |

| Online Term Loans & Lines of Credit | Working capital and inventory purchases | $5K-$500K | 24-72 Hours | Fast approvals, minimal paperwork, unsecured options | Higher interest rates, frequent repayment schedules |

| Business Credit Cards & 0% APR Stacking | Marketing, startup expenses, short-term cash flow | $10K-$100K+ | Same Day | 0% financing options, rewards, easy access | Personal guarantee, rates spike after intro period |

| Private Money Lending | Real estate investors, construction, asset-backed projects | $50K-$5M | 1-3 Weeks | Flexible terms, asset-based underwriting, fast closings | Higher rates than banks, collateral required |

| Equipment Financing | Equipment, vehicles, machinery purchases | Up to 100% of equipment cost | 1-2 Weeks | High approval rates, preserves cash, tax benefits | Limited to equipment purchases only |

| Crowdfunding & Community Capital | Startups, consumer products, innovative ideas | $10K-$5M | 30-60 Days | No loan payments, market validation, built-in marketing | Time-intensive, public campaign risk, platform fees |

| Grants & Government Programs | R&D, minority-owned, veteran-owned, green businesses | $5K-$500K | 3-12 Months | Free money, no repayment, no equity dilution | Extremely competitive, lengthy application process |

Funding Speed Comparison

Which Funding Option Is Best?

| Situation | Recommended Funding |

|---|---|

| Need money this week | Business Credit Cards, Online Loans, RBF |

| Real Estate Investment | Private Money Lending |

| Equipment Purchase | Equipment Financing |

| Lowest Interest Rate | SBA Loan |

| Startup with No Revenue | Crowdfunding, Grants |

| SaaS or Subscription Business | Revenue-Based Financing |

| Manufacturing Expansion | SBA 504 or Equipment Financing |

| Fix & Flip Project | Private Money Lending |

| Ground-Up Construction | Private Money Lending |

| Marketing Campaign | 0% APR Business Credit Cards |

Overall Rankings

Best Overall Cost: SBA Loans

Fastest Funding: Business Credit Cards

Most Flexible: Private Money Lending

Best for Real Estate Investors: Private Money Lending

Best for SaaS & E-commerce: Revenue-Based Financing

Best Free Capital: Grants

Best Startup Funding: Crowdfunding

Best Equipment Purchases: Equipment Financing

For your audience at Medex PMC, the strongest comparison is usually SBA Loans vs Private Money Lending vs Revenue-Based Financing, because those are the three options most real estate investors and small business owners evaluate when trying to fund acquisitions, construction projects, or business expansion.

Funding Speed Comparison

Approximate time to receive funding.

| option | days |

|---|---|

| Business Credit Cards | 1 |

| Online Loans | 3 |

| Revenue-Based Financing | 5 |

| Equipment Financing | 10 |

| Private Money Lending | 14 |

| Crowdfunding | 45 |

| SBA Loans | 75 |

| Grants | 180 |

FAQ: Small Business Financing Options 2026

What’s the easiest business funding to get in 2026?

Business credit cards or Fundbox lines—24-hour approvals if credit’s decent. No deep dives.

Can I get business funding with bad credit?

Yes: RBF (revenue rules), equipment financing (asset focus), invoice factoring. Avoid personal guarantees.

How is revenue-based financing different from a loan?

No fixed payments—percentage of sales. Aligns with cash flow, no default if revenue dips.

Is private money lending safe for small businesses?

Safe with due diligence: Vet lenders, secure assets legally. Flexible but rates higher—use for speed.

What credit score do I need for SBA loans?

Typically 680+, but 620 workable with strong financials/collateral.

How long does business funding take in 2026?

Hours (cards), 1-3 days (online/RBF), weeks (private/equipment), months (SBA/grants).

Can a startup get funding without revenue?

Crowdfunding, grants, or strong personal credit cards. RBF needs traction.

What documents do I need to apply for business funding?

Bank statements (3-6 mo), tax returns (2 yrs), P&L, ID. Revenue lenders want API access.

Key Takeaways from the 2026 Small Business Funding Roadmap

- Skip banks: 8 alternatives fit every speed/revenue profile.

- Use the four-step framework—speed, quals, cost, purpose.

- Avoid traps: Shop rates, match debt to ROI, watch guarantees.

- 2026 edge: AI, embedded finance—get your books AI-ready now.

- Action first: Audit your fit today.

Your Next Move: Chart the Roadmap

The old bank-only path is dead. Your small business funding roadmap for 2026 puts control back in your hands—faster capital, smarter terms, real growth.

Pick one path, run the framework, apply tomorrow.

Explore our guides on business credit cards, unsecured loans, and accounting software to stack your funding arsenal.

Fund smarter. Grow faster.

What is the $10 000 SBA grant?

The $10,000 SBA grant refers to the Economic Injury Disaster Loan (EIDL) Advance provided by the Small Business Administration (SBA) during the COVID-19 pandemic. This grant was aimed at helping small businesses cover immediate operational costs and was intended to be fast-tracked for applicants affected by the economic downturn. Eligible businesses could receive up to $10,000 without needing to repay it.

Can an LLC get grant funding?

Yes, an LLC can apply for grant funding, provided it meets the eligibility requirements set by the grantor.

What is the monthly payment on a $50,000 business loan?

The monthly payment on a $50,000 business loan depends on the interest rate and the loan term. Use this formula to calculate monthly payments:

\[ M = P \times \frac{r(1 + r)^n}{(1 + r)^n – 1} \]

Where:

– \( M \) = monthly payment

– \( P \) = loan amount ($50,000)

– \( r \) = monthly interest rate (annual rate / 12)

– \( n \) = number of payments (loan term in months)

For example, if the interest rate is 5% per annum for 5 years:

Monthly interest rate (r) = 0.05 / 12 = 0.004167

Number of payments (n) = 5 years × 12 months/year = 60

Plug in the values:

\[ M = 50000 \times \frac{0.004167(1 + 0.004167)^{60}}{(1 + 0.004167)^{60} – 1} \]

Calculate \( M \) to find the monthly payment.

Can a new LLC get funding?

Yes, a new LLC can get funding through various sources such as personal savings, loans, angel investors, venture capital, crowdfunding, or grants.