Columbia, SC, is rapidly emerging as a premier destination for entrepreneurs, commercial investors, and developers. With its strategic location, robust population growth, and a business-friendly environment, the capital of South Carolina offers a unique landscape for those looking to scale. Whether you are a local business owner looking to expand or an investor eyeing the next big commercial real estate opportunity, understanding the nuances of commercial lending in Columbia, SC, is the first step toward success.

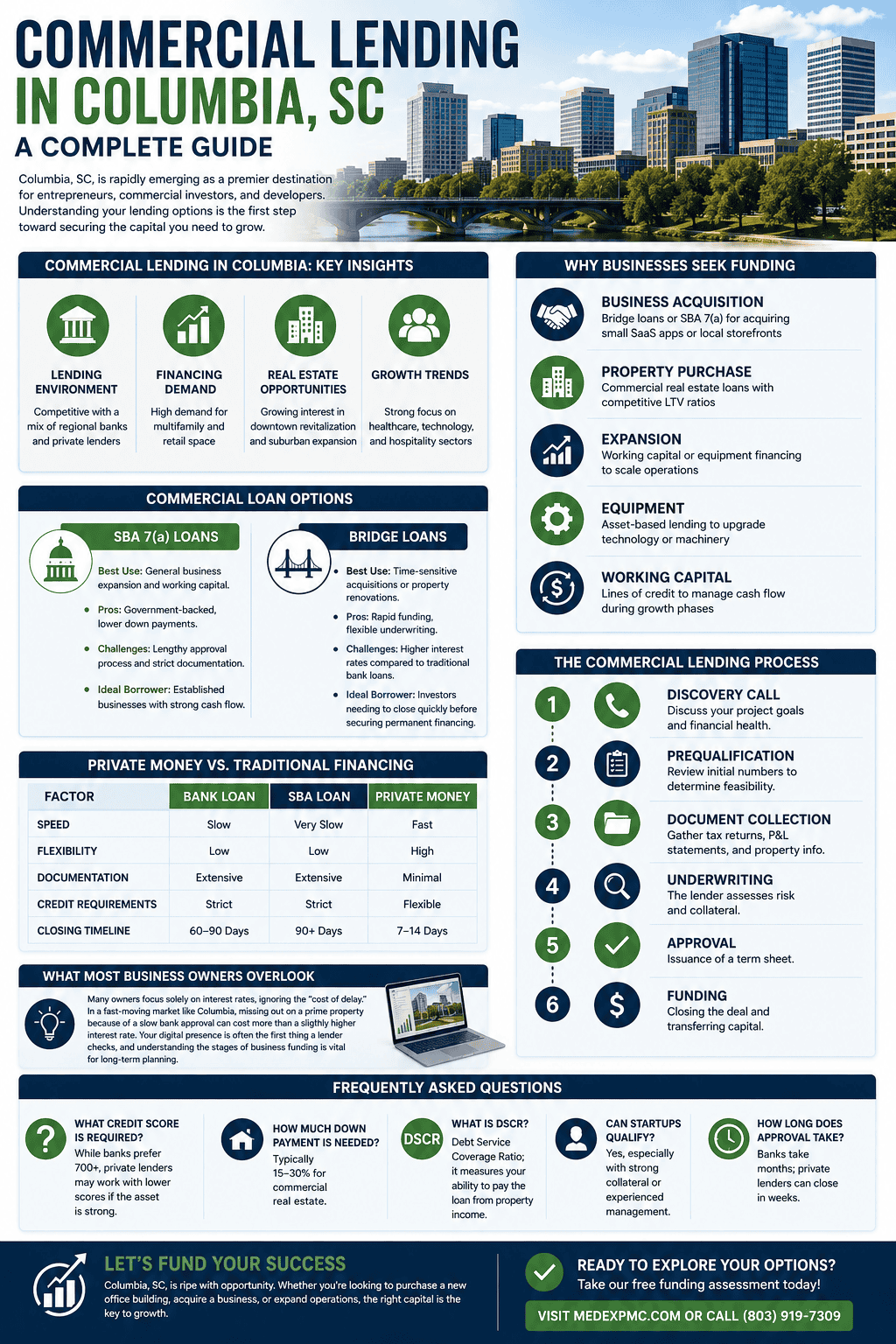

Commercial Lending in Columbia: A Complete Guide

Navigating the local lending environment requires a clear understanding of the demand for capital and the specific growth trends defining the region.

| Factor | Local Insight |

|---|---|

| Lending Environment | Competitive with a mix of regional banks and private lenders |

| Financing Demand | High demand for multifamily and retail space |

| Real Estate Opportunities | Growing interest in downtown revitalization and suburban expansion |

| Growth Trends | Strong focus on healthcare, technology, and hospitality sectors |

Why Businesses Seek Funding

Securing the right capital is essential for long-term sustainability. Many business owners in Columbia find themselves at a crossroads where traditional funding is either too slow or too restrictive.

| Business Goal | Typical Funding Need |

|---|---|

| Business Acquisition | Bridge loans or SBA 7(a) for acquiring small SaaS apps or local storefronts |

| Property Purchase | Commercial real estate loans with competitive LTV ratios |

| Expansion | Working capital or equipment financing to scale operations |

| Equipment | Asset-based lending to upgrade technology or machinery |

| Working Capital | Lines of credit to manage cash flow during growth phases |

Commercial Loan Options

SBA 7(a) Loans

- Best Use: General business expansion and working capital.

- Pros: Government-backed, lower down payments.

- Challenges: Lengthy approval process and strict documentation.

- Ideal Borrower: Established businesses with strong cash flow.

Bridge Loans

- Best Use: Time-sensitive acquisitions or property renovations.

- Pros: Rapid funding, flexible underwriting.

- Challenges: Higher interest rates compared to traditional bank loans.

- Ideal Borrower: Investors needing to close quickly before securing permanent financing.

Private Money vs. Traditional Financing

When time is of the essence, private money often serves as a bridge to success. Unlike traditional banks, private lenders focus more on the asset value and the potential of the project rather than just historical credit scores.

| Factor | Bank Loan | SBA Loan | Private Money |

|---|---|---|---|

| Speed | Slow | Very Slow | Fast |

| Flexibility | Low | Low | High |

| Documentation | Extensive | Extensive | Minimal |

| Credit Requirements | Strict | Strict | Flexible |

| Closing Timeline | 60-90 Days | 90+ Days | 7-14 Days |

The Commercial Lending Process

- Discovery Call: Discuss your project goals and financial health.

- Prequalification: Review initial numbers to determine feasibility.

- Document Collection: Gather tax returns, P&L statements, and property info.

- Underwriting: The lender assesses risk and collateral.

- Approval: Issuance of a term sheet.

- Funding: Closing the deal and transferring capital.

What Most Business Owners Overlook

Many owners focus solely on interest rates, ignoring the “cost of delay.” In a fast-moving market like Columbia, missing out on a prime property because of a slow bank approval can cost more than a slightly higher interest rate. Proper website maintenance and SEO are also critical; your digital presence is often the first thing a lender checks to verify your business legitimacy. Furthermore, understanding the stages of business funding is vital for long-term planning.

Here are four additional sections that will make the article more authoritative, increase time on page, and create more opportunities to rank for commercial lending-related searches.

Real-World Commercial Lending Columbia SC Case Studies

The following examples illustrate how different financing solutions can help businesses and investors move forward. These scenarios are for educational purposes but reflect common lending situations seen throughout the Columbia market.

Case Study 1: Purchasing a Small Office Building

A professional services firm wanted to purchase the office building it had been leasing for years. Rather than continuing to pay rent, the owners secured a commercial real estate loan that allowed them to build equity while locking in predictable monthly payments.

Project: Owner-occupied office building

Purchase Price: $1.8 million

Financing: Commercial mortgage

Result: Long-term ownership with stable occupancy costs and increased business equity.

Case Study 2: Bridge Loan for a Retail Center

An investor located a neighborhood retail center with several vacant suites. The seller required a quick closing, making traditional bank financing too slow.

The investor used a bridge loan to acquire the property, completed renovations, leased the vacant spaces, and later refinanced into permanent financing.

Purchase Price: $4.2 million

Loan Type: Bridge Loan

Closing Time: Approximately 12 days

Outcome: Increased occupancy and long-term refinancing after stabilization.

Case Study 3: Manufacturing Equipment Expansion

A growing manufacturer needed new production equipment to fulfill larger contracts.

Instead of using working capital, the company financed the equipment, preserving cash for payroll and inventory while increasing production capacity.

Funding Type: Equipment Financing

Purpose: Production expansion

Result: Increased revenue without draining operating cash.

Case Study 4: Multifamily Acquisition

A real estate investor acquired a 32-unit apartment community using private financing while improvements were completed.

After renovations increased rental income, the property qualified for permanent financing with more favorable long-term terms.

Property Type: Multifamily

Strategy: Value-add investment

Exit Strategy: Refinance after stabilization.

Comparing Commercial Loan Types

Every financing option serves a different purpose. Choosing the right loan often depends on your timeline, property type, and long-term investment strategy.

| Loan Type | Best For | Typical Timeline | Primary Advantage |

|---|---|---|---|

| Commercial Mortgage | Buying or refinancing commercial property | 45–90 days | Lower long-term interest rates |

| SBA 7(a) Loan | Business acquisition and working capital | 60–120 days | Government-backed financing |

| Bridge Loan | Time-sensitive purchases | 7–21 days | Fast closings |

| Private Money | Investment opportunities requiring flexibility | 5–14 days | Flexible underwriting |

| Equipment Financing | Machinery and technology | 1–4 weeks | Preserve working capital |

| Line of Credit | Ongoing cash flow | 2–6 weeks | Access funds when needed |

Rather than asking which loan is “best,” ask which loan best fits your current stage of growth.

Common Reasons Commercial Loans Columbia SC Are Declined

Many applicants assume credit score is the deciding factor. In reality, lenders evaluate the complete picture.

Some of the most common reasons commercial loan applications are denied include:

- Inadequate cash flow to support debt payments

- Insufficient borrower equity

- Weak collateral value

- Poorly documented financial statements

- No clear business plan or exit strategy

- Unrealistic property valuations

- Environmental or title issues

- Limited management experience for complex projects

Addressing these issues before submitting an application can significantly improve the likelihood of approval.

Preparing Your Business Before Applying

The strongest borrowers often begin preparing months before they apply for financing.

Lenders generally expect organized documentation, realistic financial projections, and a clear understanding of how the requested capital will be used.

Before requesting financing, consider assembling:

- Three years of business and personal tax returns

- Current profit and loss statement

- Balance sheet

- Business bank statements

- Personal financial statement

- Business plan or executive summary

- Property information (if purchasing real estate)

- Existing debt schedule

- Rent rolls or leases for investment properties

- Purchase contract or letter of intent

- Organizational documents for your LLC or corporation

Having these items prepared in advance can speed underwriting and reduce delays during the approval process.

These sections also give you additional opportunities to rank for long-tail keywords such as:

- commercial loan case studies

- commercial lending examples

- types of commercial loans

- commercial loan comparison

- why commercial loans get denied

- commercial loan application checklist

- bridge loan vs commercial mortgage

- private money vs bank financing

- commercial real estate financing Columbia SC

Frequently Asked Questions

- What credit score is required? While banks prefer 700+, private lenders may work with lower scores if the asset is strong.

- How much down payment is needed? Typically 15-30% for commercial real estate.

- What is DSCR? Debt Service Coverage Ratio; it measures your ability to pay the loan from property income.

- Can startups qualify? Yes, especially with strong collateral or experienced management.

- How long does approval take? Banks take months; private lenders can close in weeks.

Conclusion

Columbia, SC, is ripe with opportunity. Whether you are looking to purchase a new office building or expand your existing operations, having access to the right capital is the key to growth. If you’re considering a commercial property purchase, business acquisition, investment opportunity, or expansion project in Columbia, take our free funding assessment to explore your options.